During the 2008 housing crisis, home prices plummeted by an average of 33% nationwide, catching many real estate investors off guard. This stark reality underscores the critical link between economic recessions and the housing market. As an investor, understanding this relationship can mean the difference between substantial losses and strategic gains. This article digs into the nitty-gritty of how recessions shape housing trends, offering you a comprehensive look at historical patterns, current market dynamics, and practical strategies to navigate uncertain times. You'll get the lowdown on past recessions, including the 2008 meltdown, and how they've impacted everything from property values to mortgage rates. But we won't just leave you with history lessons. You'll walk away with actionable advice for both buying and selling in a recession-impacted market, empowering you to make data-driven decisions that could potentially safeguard your investments. Ready to turn economic uncertainty into your competitive edge in real estate?

Recession Basics and Housing Market Sensitivity

Recession Basics and Housing Market Sensitivity

Two consecutive quarters of declining Gross Domestic Product (GDP) mark the technical start of an economic downturn. These periods bring widespread changes across industries – manufacturing slows, retail sales decrease, and businesses reduce their workforce. The ripple effects touch every sector, from small local shops to large corporations, creating a cycle where reduced spending leads to decreased production and employment.

Financial institutions respond by adjusting their lending practices, often making credit harder to obtain. Companies scale back operations, leading to increased unemployment rates. This creates a domino effect where consumer spending drops further, affecting everything from luxury goods to essential services. The manufacturing sector typically experiences immediate impacts, while service industries feel the effects gradually.

Property Market Dynamics During Economic Shifts

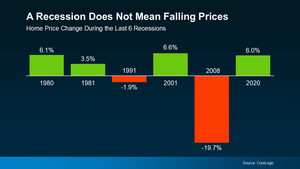

The real estate sector responds distinctively to economic pressures. Home prices don't actually fall much during recessions, contrary to common belief. The 2008 housing crash stands as an exception rather than a standard outcome. Property values tend to stabilize rather than plummet, influenced by the basic principle of supply meeting actual housing needs rather than speculative demand.

Mortgage rates become a crucial factor during these periods, with current projections showing rates between 6.5% to 7.25% in 2025. These figures significantly influence buying power and market accessibility. Lenders typically tighten their qualification requirements, making it more challenging for potential buyers to secure financing. This creates a selective market where financially stable buyers often find increased negotiating power due to reduced competition.

Mortgage rates become a crucial factor during these periods, with current projections showing rates between 6.5% to 7.25% in 2025. These figures significantly influence buying power and market accessibility. Lenders typically tighten their qualification requirements, making it more challenging for potential buyers to secure financing. This creates a selective market where financially stable buyers often find increased negotiating power due to reduced competition.

Consumer sentiment plays a defining role in market behavior. When retirement accounts shrink and job security wavers, potential buyers often postpone major purchases. This psychological factor, combined with actual financial constraints, shapes market activity more than pure economic indicators. The relationship between buyer confidence and market movement creates opportunities for investors who maintain strong financial positions during downturns.

Monitoring interest rate movements provides critical insights for timing investment decisions. Rates respond to Federal Reserve policies aimed at managing economic stability. Understanding these patterns helps investors position themselves advantageously, whether for property acquisition or portfolio adjustment. Local market conditions often diverge from national trends, creating pockets of opportunity in specific regions or property segments.

Historical Patterns and Lessons from Past Recessions

The 2008 real estate market crash sent property values plummeting by 27.4% nationally over a six years. Some regions experienced devastating losses reaching 50% of property values, marking the most severe housing downturn in modern history. Mortgage-backed securities and risky lending practices fueled a speculative bubble that, when burst, triggered widespread foreclosures and market instability.

Fast forward to 2020, and the COVID-19 recession painted a drastically different picture. Despite initial fears of market collapse, property values remained surprisingly stable and even increased in many areas. This stark contrast to 2008 stemmed from stronger lending standards, better-qualified buyers, and swift government intervention through monetary policy and support programs.

Key lessons from these contrasting market scenarios reveal critical insights for investors:

- Responsible lending practices significantly impact market stability - risky lending makes the downturn worse

- Local market conditions often deviate from national trends, creating targeted investment opportunities

- Government policy responses shape recovery speed and market resilience

- Property values typically recover faster in areas with diverse economic drivers

- Cash reserves and strong credit positions become crucial during market corrections

- Market corrections create opportunities for well-positioned buyers

- Different types of properties respond uniquely to economic pressures

Studying these historical patterns reveals that demand will return after market corrections. Strategic investors who maintain strong financial positions during downturns often find opportunities to acquire properties at favorable prices, particularly in markets with solid economic fundamentals and growth potential. The key lies in recognizing that each recession brings unique challenges and opportunities, requiring adaptable strategies rather than rigid approaches based solely on past experiences.

Analyzing Current Housing Market Conditions

Property prices rose 4.8% year-over-year in the fourth quarter of 2023, defying predictions of a market slowdown. Available homes for sale remain at historic lows, with only 1.5 months of supply nationwide compared to the balanced market standard of 6 months. This scarcity continues to drive competitive bidding situations, particularly in mid-sized metropolitan areas where job growth remains strong.

Construction costs have jumped 15% since 2021, forcing builders to focus on higher-margin properties rather than entry-level homes. The resulting shortage of affordable housing options has created intense competition among first-time buyers, who now make up 45% of all purchase applications. Monthly mortgage payments take up an average of 33% of household income, stretching beyond the recommended 28% threshold for financial stability.

Key factors reshaping buyer demographics and market demand include:

- Millennials entering peak homebuying years, with 4.8 million turning 34 in 2024 alone

- Remote work policies expanding viable commuting zones, spreading demand to suburban areas

- Baby boomers aging in place longer, reducing natural market turnover by 25%

- Investment firms purchasing 1 in 5 starter homes, adding pressure to entry-level inventory

- Rising student debt delaying first-time purchases by an average of 7 years

- Multi-generational households increasing by 30%, creating demand for larger properties

Geographic price variations show stark differences across regions. Southeastern states report 8-12% annual appreciation, while Western markets see modest 2-3% gains. Mid-sized cities with strong tech sectors command premium prices, yet rural areas within 2 hours of major employment hubs demonstrate accelerating growth as buyers seek affordability.

Monitoring local employment data proves essential for identifying market stability. Areas with diverse job sectors and growing wages show consistent price appreciation, while regions dependent on single industries face higher volatility. Population migration patterns between states create ripple effects, with some markets experiencing sudden surges in demand while others face unexpected softening.

Mortgage Rates and Economic Downturns

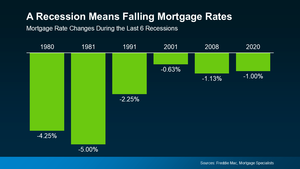

The Federal Reserve's monetary policy decisions directly shape borrowing costs across financial markets. During past economic slowdowns, the Fed has consistently lowered benchmark interest rates to boost economic activity. This pattern shows up clearly in mortgage rate data, with the 30-year fixed rate typically falling during recessionary periods since the 1980s. These rate adjustments create significant shifts in the real estate financing landscape.

Banks and lending institutions respond to broader economic pressures by adjusting their loan terms and qualification standards. When businesses scale back operations and unemployment rises, overall demand for mortgage financing decreases. The yield on 10-year Treasury bonds, a key benchmark for mortgage rates, often drops as investors seek safer assets. Financial institutions then compete more aggressively for qualified borrowers, leading to more favorable lending terms despite tighter qualification requirements.

Lower borrowing costs create opportunities for strategic property purchases. A 1% decrease in mortgage rates can boost purchasing power by approximately $30,000 on a median-priced home. First-time buyers often find improved affordability during these periods, especially in markets where property values have stabilized. Cash buyers and investors with strong credit profiles gain additional leverage in negotiations, while sellers become more willing to consider creative financing options to close deals.

Predicting rate movements requires analyzing multiple economic indicators. Mortgage rates rose from 2.95% to 5.55% between early 2021 and August 2022, demonstrating how quickly market conditions can shift. Employment levels, inflation data, and global economic factors will continue influencing future rate trends. Property investors who track these metrics position themselves to capitalize on favorable financing windows while maintaining flexibility in their investment strategies.

Strategic Tips for Navigating the Market

Mortgage rates between 6.5% and 7.25% create unique buying windows for savvy investors who understand market dynamics. Smart buyers capitalize on seasonal price fluctuations, with winter months showing 5-7% lower purchase prices compared to peak summer periods. This data-backed pattern provides clear advantages for buyers willing to move against typical purchase cycles.

Key action steps for buyers seeking optimal purchase conditions:

- Schedule property viewings during off-peak hours - Tuesday through Thursday showings face 23% less competition

- Submit offers during the first week of January when seller motivation peaks and competition drops

- Request detailed property condition reports and maintenance records from the past 5 years

- Calculate price-to-rent ratios for neighboring properties to validate investment potential

- Secure mortgage pre-approval 90 days before planned purchases to leverage rate locks

- Review comparable sales from the previous 6 months to identify pricing trends

- Build relationships with 3-4 local agents who specialize in distressed properties

- Monitor days-on-market statistics to identify properties ripe for negotiation

Sellers face different challenges when timing their market entry. Properties listed in March through May typically sell 15% faster and command 2-3% higher prices than winter listings. Smart pricing strategies start with a professional appraisal, followed by weekly reviews of new listings and sales in the immediate area. Successful sellers price within 2% of recent comparable sales, adjusting weekly based on showing feedback and market response.

Property preparation makes a measurable difference in sale outcomes. Fresh paint and basic repairs deliver a 3-to-1 return on investment. Professional photos increase online viewing time by 45% and drive more qualified showings. Sellers who stage key living areas report 15-20% faster sales at prices 5-7% above non-staged properties.

Managing financial risk requires maintaining six months of carrying costs in liquid reserves. This buffer protects against market shifts and provides negotiating leverage during transactions. Diversifying across property types and locations reduces exposure to local market fluctuations. Regular portfolio reviews help identify properties that no longer meet performance targets, enabling strategic exits before market conditions change.

Final Thoughts

Recessions reshape housing markets in predictable ways, as shown by patterns from past economic downturns like the 2008 crisis. These market shifts create both risks and opportunities for buyers and sellers. The data shows that property values often decrease during recessions, mortgage rates fluctuate, and buyer behavior changes significantly. Yet smart investors can use this knowledge to their advantage.

Understanding these patterns helps you make better real estate decisions. You'll spot potential deals when others panic-sell, recognize when to hold properties for long-term appreciation, and know which market indicators signal upcoming changes. The strategies we've covered work for both individual homeowners and professional investors - from timing purchases during market dips to negotiating better terms with motivated sellers.

Your next steps should focus on practical action. Start by reviewing local market data, particularly in areas you're interested in investing. Build relationships with real estate agents who have experience handling transactions during previous recessions. Keep track of key economic indicators that typically predict housing market changes. Most importantly, maintain a cash reserve to act quickly when opportunities arise. The housing market will always have ups and downs, but informed investors consistently find ways to succeed, regardless of economic conditions.